Bentsifi’s Tattle – Guy about town

The quiet architect of modern African art There are people who chase the spotlight. Then there are those …

Bentsifi’s Tattle – Guy about town

Under the Odum…with Tamara Jonah award-winning hospitality entrepreneur, creative director, and experience architect Founder and CEO of …

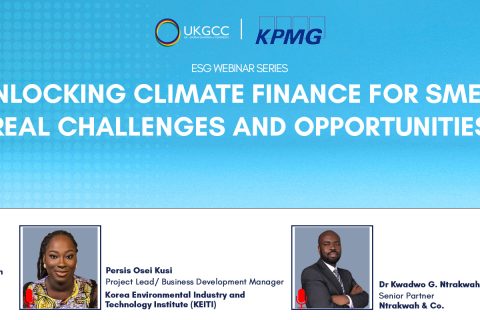

Investment readiness, not funding, is the biggest barrier to climate finance for SMEs

Investment readiness, rather than the availability of finance, remains one of the biggest barriers preventing small and medium-sized …

GRA to automate treaty benefit applications amid major international and local tax reforms

The Head of the Ghana Revenue Authority’s (GRA) International Tax Office, Nana Mensah Otoo Esq., says the GRA …

Investors increasingly using ESG to shape investment decisions in Africa

Environmental, Social and Governance (ESG) considerations are increasingly shaping how capital is deployed across Africa, with investors looking …

Bentsifi’s Tattle…Guy about town

The Economy Of Trust Redefining Ghana’s Tourism Through GTIS – In an industry where visibility is currency, will …

UKGCC and AmCham strike a chord for charity at international jazz day commemoration

The UK-Ghana Chamber of Commerce (UKGCC), in collaboration with the American Chamber of Commerce-Ghana (AmCham Ghana), has hosted a vibrant and …

Ghana High Commission invites global investors to the Ghana-UK investment summit 2026

The Ghana High Commission to the United Kingdom and Republic of Ireland proudly announces the Ghana-UK Investment Summit …

Blue Skies urges media to highlight responsible businesses on World Press Freedom Day

The Head of Corporate Affairs and Foundation at Blue Skies Products (Ghana) LTD., Mr Alistair Djimatey, has called …

New tax updates in Ghana bring relief to businesses

Businesses in Ghana are beginning to feel a sense of relief following recent tax updates, a development that …